Last week was certainly an interesting one for the markets, both here in the U.S and globally. I’d like to believe that the markets are beginning to emerge from the trading range they’ve been stuck in for the last few months, but I just can’t convince myself that the tides have changed, at least not completely. Although I will concede that buying opportunities are emerging, especially considering the number of upgrades in my analysis this morning.

There are now ten major markets that I analyze (I added two over the weekend), yet none pass both the proprietary alpha analytic and the confirming technical indicators tests needed to be recommended “buys.” However, eight of the ten are “neutral” rated, with only the S&P Small Cap (IJR) and S&P Mid Cap (IJH) markets currently rated “sell.” The top two major markets are the NYSE (NYC) and the S&P 500 (IVV). Investors looking for broad-based market exposure in their portfolios might look to those two Exchange Traded Funds first.

Of the ten “style-box” investments that I analyze, I still see no outright recommended “buys” although there are seven “neutral” rated derivatives. The Russell 3000 Growth (IWW) and S&P Large Cap Value (IVE) are at the top of the “neutral” rated style-box investments. A lot of investors, when developing and managing their long-term portfolios, like to allocate based on style-box, which is one of the reasons we include this analysis in our Market Overview section of the newsletter. What today’s analysis should tell them is that there are no style-boxes that are clearly out-performing the others, so there is no need to adjust asset allocation yet. However, they should pay special attention over the next few days and see if any style-box derivative emerges as a market leader.

The Sector analysis is where things are getting interesting. We still have only four “buy” rated sectors including Real Estate (IYR), Utilities (IDU), Healthcare (IYH) and Telecommunication (IYZ). Real Estate and Utilities have been “buys” for a few weeks now and have done very well in the face of a highly volatile market, while Healthcare and more recently Telecommunication have done well in the near-term. And although I’m not seeing any obvious weakening in these sectors, I think there are others that warrant some attention.

Obviously Energy (IYE) and Natural Resources (IGE) are in play with the turmoil in the Middle East, rising gas prices and the U.S. heat wave. Most, if not all investors should have at least one holding in energy at this point, so this is not really new knowledge.

What I’m interested in are Financials (IYF), Financial Services (IYG) and Non-Cyclicals (IYK), as these very well might be the leading sectors within the next few weeks. Bear Stearns Companies Inc. (BSC) and Merrill Lynch & Co. Inc. (MER) were upgraded to “buys” this morning.

Additionally, I think Semiconductors (IGW) are worth examining. It is the lowest rated “neutral” sector currently, but was the best performing last week. With the NASDAQ taking a beating recently, a speculative holding in a recently upgraded semiconductor company, such as Novellus Systems Inc. (NVLS); Micrel Inc. (MCRL) or Microsemi Corp. (MSCC) might be worth looking into.

Each week I provide a graph of six holdings from the Alpha Advisor Service, LLC newsletter. Included in the letter, which is provided to our subscribers on Tuesday and Thursday mornings, is the Top Ten page. The Top Ten page is broken down into six groups of equities that include: Long Stocks, Short Stocks, Exchange Traded Funds, Fidelity Select Funds, ProFunds Funds and Rydex Funds. We include ten equities within each group, ranked first by the current AAS Recommendation, and then by the AAS Rating Score. Those that are “AAS Recommended Buys” and that have the highest AAS Rating Scores are at the top. The graphs below represent the top holding within each of the six groups as of Friday, July 21, 2006. I’ve included the date that the equity was most recently labeled an “AAS Recommended Buy,” or in the case of the short-sell group, an “AAS Recommended Sell.” I’ve also included the current recommendation of each security.

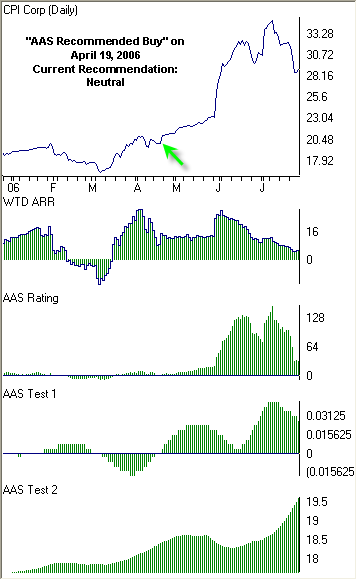

CPI Corp. (CPY) was the highest rated stock within the “Long Stock” group as of July 21, 2006. CPY was upgraded to an “AAS Recommended Buy” on April 19, 2006 at a dividend-adjusted price of 20.87 (the company paid a $0.16 dividend on May 18, 2006). It shifted from an “AAS Recommended Buy” to an “AAS Recommended Neutral” on July 24, 2006. Since being up-graded to an “AAS Recommended Buy,” CPY is up 38.24%.

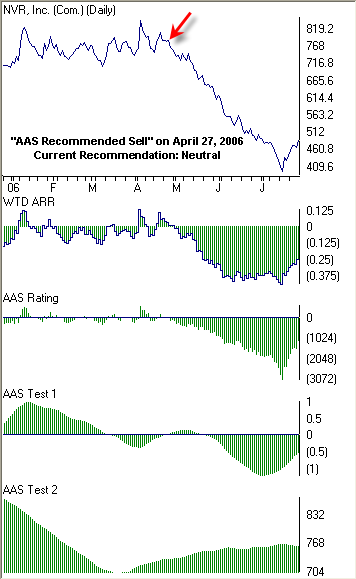

For the second week in a row, NVR Inc. (NVR) was the highest rated stock within the “Short Stock” group. This group includes those securities that are “AAS Recommended Sells” and that have the lowest AAS Rating Scores. This group is included in the newsletter for those investors looking to add alpha to their portfolios by shorting companies. NVR became an “AAS Recommended Sell” on April 27, 2006 at a price of 763.00 and closed at 484.49 on Friday, July 28th for a loss of -36.50%. Currently, NVR is an “AAS Recommended Neutral.” Shorting stocks, although profitable if done correctly, is risky business. There's no need to do it unless you have the experience, knowledge, and capital to cover your short if needed. QMA does not short stocks for its clients and AAS does not recommend the practice to its subscribers.

The iShares Cohen and Steers Realty Majors ETF (ICF) was the highest rated Exchange Traded Fund for the second week in a row. It was up-graded to an "AAS Recommended Buy" on June 29, 2006. As of the close on Friday, July 28th, ICF has gone up 5.83% and currently remains an "AAS Recommended Buy."

Healthcare, Utilities, Telecommunication and Real Estate have been the only four “AAS Recommended Sectors” over the last few weeks. As such, the Fidelity Select Healthcare Fund (FSPHX) was this highest rated Fidelity Select mutual fund as of July 21, 2006. It was upgraded to an “AAS Recommended Buy” on July 20, 2006 at a price of 119.32. As of the close on Friday, July 28th, FSPHX has gone up 3.31% and currently remains an “AAS Recommended Buy.”

The ProFunds Ultra Short OTC Fund (USPIX) was again the highest rated ProFund mutual fund for the week ending July 21, 2006. This fund is leveraged to correspond to twice the inverse of the NASDAQ 100 Index and has out-performed because of the recent weakness in the tech sectors. USPIX was upgraded to an "AAS Recommended Buy" on July 5th when the price was 17.48. As of Friday, July 28th, USPIX closed at 18.50 for a gain of 5.84%. Because of the past weeks market activity, and the potential strengthening of the tech sectors, USPIX is now an "AAS Recommended Neutral."

Again, the Rydex Inverse Dynamic OTC Fund (RYVNX) was the highest rated Rydex mutual fund for the week ending July 21, 2006. This fund is also leveraged to correspond to twice the inverse of the NASDAQ 100 Index. RYVNX was upgraded to an "AAS Recommended Buy" on July 6th at a price of 22.19. As of Friday, July 28th, the close was 23.43 for a gain of over 5.59%. Similar to its ProFund counterpart above, RYVNX is now an "AAS Recommended Neutral."

A lot of investors have heard about portable alpha, yet are confused about what it means or how it works. It’s really quite a simple theory, but one that is unfortunately thought to be limited to hedge funds and other investments available for only wealthy investors. I came across this article last night by Scott Patterson of the Wall Street Journal. He outlines the debate regarding portable alpha, explaining the perceived pros and cons of it in the eyes of professional investors. Although he makes some good points, there is another aspect of portable alpha that Scott and a lot of other people don’t address. The fact is that portable alpha can be used by anyone, inside any portfolio, and that investors wanting to invest in it don’t need a hedge fund to do it.

Investors seeking to add alpha to their portfolios can do so in a variety of ways. The most basic method involves investing in a market derivative that provides enough exposure so that the portfolio at least stays on par with the market. Hedge funds use a lot of complicated put / call options and leverage to do this, but that’s not the only method. In fact, average investors can get adequate market exposure by investing in an ETF of a broad-based index, such as IVV, which is an iShare “derivative” correlated to the S&P 500. Granted, iShares such as IVV are not correlated 100% to the S&P 500, and typically trade at lower volume than index mutual funds. But they are much cheaper, which is a crucial component of investing in portable alpha. With adequate exposure to the overall market at a lower cost, investors can then allocate the capital saved by investing in the index derivative into other areas of the market, such as sectors, bonds or specific equities.

So how does the average investor wanting to invest in portable alpha start today? I’m going to answer that question and shift my future posts in this direction instead of focusing on the indicators I use and our allocation recommendations.

Currently, of the eight major markets I analyze each morning, none pass all of the tests in order to be recommended “buys.” Four of them however, are “neutral” rated, meaning they pass about half of the tests, but need more time to strengthen before they can be upgraded. Those three include the NYSE Composite (NYC); the Dow Jones Industrial Average (IYY) and the S&P 500 (IVV). So the first step in investing in portable alpha involves determining the health of the broad-based markets. If you feel comfortable with a specific market and want exposure to it inside your portfolio, look for a derivative that mimics the market, such as an iShare or other ETF.

Taking the market analysis one step further involves style-box investments. Again, there are no “buys” this morning, but the Russell 3000 Growth (IWW) and S&P Large Cap Value (IVE) are rated “neutral.” Assuming you’re comfortable with the overall health of the market (thanks to step #1), the second step in investing in portable alpha consists of determining whether value, growth or all-style equities are out-performing and which market cap.

The third step is determining which sectors are currently outperforming the market. For example, four sectors out of the eighteen that I analyze are rated as “buys” today. These include Real Estate (IYR), Utilities (IDU), Telecommunication (IYZ) and Healthcare (IYH).

At this point, you now have several options. You can invest in the iShare itself of the sector(s) you like. Or you can look for a sector-specific mutual fund. You can also invest in a specific company that falls within the sector(s) you chose.

Here’s an example of how I would set up an investment portfolio based on this mornings analysis. The S&P 500 (IVV) is rated “neutral.” It has a positive, yet low rating score, which means it’s just beginning to develop a bullish trend. It’s not a “buy” yet, but for the sake of argument, I’d allocate 40% of my portfolio to IVV and 20% to the Dow Jones Industrials (IYY), which has a higher alpha score and a more developed trend. That leaves me with 60% of my portfolio allocated to the market in general, and 40% left over to invest in alpha. I’m not too impressed with any of the style-box investments at the moment, so I’m going to look straight at the sectors. Telecommunication (IYZ), Utilities (IDU), Real Estate (IYR) and Healthcare (IYH) are “buy” rated and have relatively newly developed trends. I’d invest 5% of my portfolio in each of those iShares.

So now I have 60% of my portfolio invested in the broad market and 20% invested in four different sectors providing adequate diversification. I have 20% left over to really find the alpha and get some pop into my portfolio.

Century Telephone Enterprises (CTL) was upgraded to a “buy” this morning, so I’d allocate 5% of my portfolio there. In terms of healthcare, Regeneron Pharmaceuticals Inc. (REGN) was also upgraded this morning, which is where another 5% of my allocation goes. This stock is especially interesting since its currently trading below its 200-Day moving average. The energy sector is solid, but natural gas is more attractive to me now than oil. I think the Fidelity Natural Gas fund (FSNGX) is a great way for me to get exposure to energy. Finally, Harmonic Lightwaves (HLIT) gets a 5% allocation not only because it’s a newly upgraded “buy” but because it gives me exposure to the tech sectors, which I don’t yet have.

The markets fell slightly short of a third straight day of gains yesterday, yet half of the short-term technical indicators I follow remained bullish. The NYSE Advance / Decline line continued to improve, as did the Dow Jones Industrial Average’s MACD and 15-Day Stochastic. Indicators weakening overnight include the DJIA 21-Day Breadth Indicator, 15-Day Relative Strength Index and 21-Day Volume Ratio as well as the S&P 500 On-Balance Volume %. This dichotomy further confirms our cautiously optimistic view of the market, which in essence sees the potential for a rally to develop over the next few weeks, but suggests patience as the indicators and market in general continue to solidify.

Volatility, as expressed by the VIX and VXN, continues to recede from both last weeks and Tuesday’s levels. The VXN remains much closer to its 52-Week high than the VIX, which should be expected based on the recent weakness in the Network, Technology and Semiconductor sectors. These sectors have been among our lowest rated sectors since at least the beginning of July. Joining those sectors at the bottom of our rating analysis is Transports, which became an “AAS Recommended Sell” sector on July 20th.

I continue to recommend an asset allocation of between 0% and 25% equities, however if we continue to see a moderately bullish trend develop, the asset allocation recommendation might be increased to between 25% and 50% equities sometime next week. The total universe of stocks, ETF and funds which I review on a daily basis is 1,742. Of those reviewed, 275 are rated "Buy," 824 are rated "Sell" and 643 "Neutral."

Those sectors which I perceive as potential leaders into a rally continue to include Real Estate, Utilities, Healthcare and Telecommunication. Sectors which have strengthened over the last few days but that fail to pass our two independent technical indicators include Energy, Natural Resources, Financials, Non-Cyclical, Biotechnology and Software. Investors should pay special attention to these “Neutral” rated sectors over the next few days to observe any further strengthening before investment.

Below is a list of stocks, mutual funds or exchange traded funds that were up-graded today to “AAS Recommended Buys” and that fall within one of the top four rated sectors listed above. Investors seeking to generate excess return for their portfolios might consider one or two of the following positions on a short-term basis. For information on how we analyze equities and on the proprietary alpha analytic we use, please click here.

Macerich Co. (MAC Real Estate); Peoples Energy Corp. (PGL Utilities); Mylan Laboratories Inc. (MYL Healthcare); Medtronic Inc. (MDT Healthcare); Rehabcare Group Inc. (RHB Healthcare); Owens & Minor Inc. (OMI Healthcare); Fidelity Select Medical Equipment/Systems Fund (FSEMX Healthcare); iShares S&P Global Healthcare Sector (IXJ Healthcare); Parametric Technology Corp. (PMTC Internet) and Vanguard Telecomm Services VIPERs (VOX Telecomm).

Things are beginning to get interesting on Wall Street. We’re seeing solid earnings reports, for the most part, and an earnest push by the market to at least get some traction and move forward. For the past few weeks the markets have been spinning their wheels, being driven by headlines and rhetoric and not fundamental or technical underpinnings. Still, I see no reason to shift from my bearish stance and join the bulls in a buying frenzy. Times like these, although hopefully improving, are perhaps the most dangerous in terms of letting the masses influence your investment strategy. The markets are just as likely to recede for two or three straight days as they are to improve. I suggest patience and caution over the next few days and weeks, up until the early August FOMC meeting.

I am still recommending an asset allocation of between 0% and 25% equities. The total universe of stocks, ETF and funds which Alpha Advisor Service, LLC reviews on a daily basis is 1,742. Of those reviewed, 261 are rated "Buy," 803 are rated "Sell" and 678 "Neutral." If the markets continue to gain momentum into early August, and the Fed calls for a pause in rate hikes, then we will probably shift and increase our asset allocation recommendations for the rest of the year. Until then, we’re content with the majority of our portfolios in safe investments while looking to add alpha with a few short-term holdings.

There are several arenas where investors can look to augment returns, if only for a short while. We continue to like Real Estate, Utilities, Healthcare and Telecommunication. These sectors have really performed well since they were upgraded, and most of the equities that we’ve selected within these sectors have also performed well. Other potential sectors include Energy and Natural Resources as well as Financials, which have all strengthened over the last few days, but still fall short of being “AAS Recommended Buys.” Conversely, we are avoiding Transports and Networking, which have been the lowest rated sectors for several weeks now.

Below is a list of stocks, mutual funds or exchange traded funds that were up-graded today to “AAS Recommended Buys” and that fall within one of the top four rated sectors listed above. Investors seeking to generate excess return for their portfolios might consider one or two of the following position on a short-term basis. For information on how we analyze equities and on the proprietary alpha analytic we use, please click here.

Liberty Property Trust (LRY Real Estate); PNM Resources Inc. (PNM Utilities); Cephalon Inc. (CEPH Healthcare); Hologic Inc. (HOLX Healthcare); PolyMedica Corp. (PLMD Healthcare); Biotech HOLDRs (BBH Healthcare); DSP Group Inc. (DSPG Telecommunication).

Other interesting equities upgraded this morning include:

Oracle Corp. (ORCL Internet); Merrill Lynch & Co. (MER Financials); General Mills Inc. (GIS Food); McGraw Hill Companies Inc. (MHP, Media); ProFunds Ultra Sector Biotechnology (BIPIX Biotechnology) and Aeropostale Inc. (ARO Retail).

The week started with a bang as M&A activity, positive earnings reports and a muffled Middle East sparked a broad-based rally on Wall Street. The Dow Jones Industrial Average surged 182.67, or 1.68%. The S&P 500 index gained 20.62, or 1.66% and the NASDAQ added 41.45, or 2.05%. Lower gold prices and gains for the dollar contributed to the bullish stock movement. Outside the U.S., Japan's Nikkei stock average slid 0.18% but Britain's FTSE 100 rebounded by 2%, Germany's DAX gained 2.33% and France's CAC-40 traded higher by 2%.

Better than expected earnings by Merck & Co. Inc. (MRK, “AAS Recommended Buy“) and Schering-Plough Corp. (SGP, “AAS Recommended Neutral“) combined with significant M&A activity in the form of a leveraged multibillion-dollar buyout of HCA, Inc. (HCA, “AAS Recommended Buy“) and the Advanced Micro Devices Inc. (AMD, “AAS Recommended Sell“) acquisition of ATI Technologies Inc. (ATYT, No AAS Recommendation) generated considerable optimism in the market. Strong M&A activity signals potentially strong economic growth. Bellsouth Corp. (BLS, “AAS Recommended Buy“); SanDisk Corp. (SNDK, “AAS Recommended Sell“); Kraft Foods (KFT, No AAS Recommendation); Texas Instruments (TXN, “AAS Recommended Sell“) and American Express Company (AXP, “AAS Recommended Sell“) all reported increased Q2 profits.

Today is likely the most significant day of the Q2 earnings season with five major Dow components reporting and several other big names. Altria Group Inc. (MO, “AAS Recommended Buy“), DuPont (DD, “AAS Recommended Sell“) and AT&T Inc. (T, “AAS Recommended Buy“) beat Wall Street’s estimates. McDonald’s Corp. (MCD, “AAS Recommended Neutral“) matched estimates while 3M Co. (MMM, “AAS Recommended Sell“) missed and offered cautious guidance.

The indicators that I follow continue to recommend an asset allocation of between 0% and 25% equities. The total universe of stocks, ETF and funds which Alpha Advisor Service, LLC reviews on a daily basis is 1,745. Of those reviewed, 249 are rated "Buy," 912 are rated "Sell" and 584 "Neutral." Market volatility, as expressed by the VIX and VXN, indicates ambiguity for both Bulls and Bears, neither camp entirely sure what the future holds. In addition to more earnings, economic data on consumer confidence and second-quarter gross domestic product growth could propel stocks in either direction. Seven of the eight technical indicators that I use in formulating my market view reversed direction over night, with the 9-Day Moving Average of the MACD the only one continuing a negative bias, which is to be expected.

Despite yesterday’s rally and the subsequent reversal in the indicators, I’m not yet ready to abandon my bearish allocation in favor of a head-long bullish strategy. The markets are changing direction almost daily, and I don’t believe that any sustained rally can develop prior to the Fed’s meeting on August 9th. Instead, I see the next two weeks as an opportunity for market leadership to develop in preparation of a breakthrough to the upside for the remainder of the year.

Those sectors which we perceive as potential leaders continue to include Real Estate, Utilities and Healthcare. Add to that list Telecommunication, which was upgraded this morning in large part due to positive earnings moving index components up. Several sectors, including Energy and Financials, continue to strengthen, yet fall short of being “AAS Recommended Buys.” Those sectors which we are avoiding currently include Transports, Basic Materials, Networking and Semiconductors.

Several equities within those sectors were upgraded to “AAS Recommended Buy’s” this morning. Investors should pay special attention to Essex Property Trust Inc. (ESS); Bear Sterns Companies Inc. (BSC); Allergan Inc. (AGN); Verizon Communications Inc. (VZ) and Bellsouth Corp. (BLS).

Today’s trading session opened higher as both the S&P and NASDAQ futures indicated. Already a hectic week ahead with ten Dow components reporting earnings, today’s markets will undoubtedly be further impacted by significant M&A activity as well as the weekend’s Middle Eastern activity. Advanced Micro Devices (AMD, “AAS Recommended Sell”) will acquire ATI Technologies Inc. (ATYT, No AAS Recommendation ) for $5.4 billion. Another interesting development involves what could be the largest ever leverage buyout of HCA Inc. (HCA, “AAS Recommended Buy”) for $33 billion. Shares of HCA were up 4.4% in pre-market trading. I included HCA along with Community Health Systems, Inc. (CYH, “AAS Recommended Buy”) in Friday’s post mostly because I have observed a strengthening of the Healthcare sector over the last few days and singled out these two companies since they were the newest healthcare stocks to be upgraded to “AAS Recommended Buys.” As I mentioned above, several significant earnings statements will be reported today. Companies of note releasing statements before the opening bell include Merck & Co. Inc. (MRK, “AAS Recommended Buy”) which reported a doubling of Q2 profits, BellSouth Corp. (BLS, “AAS Recommended Neutral”) and Schering-Plough Corp. (SGP, “AAS Recommended Neutral”) which both beat Wall Streets forecasts.

Other significant releases include: American Express Company (AXP, “AAS Recommended Sell”); Kraft Foods (KFT, No AAS Recommendation); SanDisk Corp. (SNDK, “AAS Recommended Sell”) and Texas Instruments (TXN, “AAS Recommended Sell”)

The technical indicators continue to point to a rather bearish market as all but one, the 15-day Stochastic, weakened after Friday’s close. Declining issues significantly outnumber advancing issues in both the NYSE and NASDAQ. Market volatility, as measured by the VIX and VXN increased slightly with Friday’s sell-off, but they remain lower than the prior week’s values. We continue to recommend an asset allocation of between 0% and 25% equities. The total universe of stocks, ETF and funds which Alpha Advisor Service, LLC reviews on a daily basis is 1,745. Of those reviewed, 189 are rated "Buy," 1047 are rated "Sell" and 509 "Neutral."

We’re still looking at the Real Estate, Utilities and Healthcare sectors as places where investors should look to invest. Currently, we see REIT equities as the most favorable real estate investment. We have twelve REIT’s rated “AAS Recommended Buy” and several of which I have mentioned in earlier posts. A newly upgraded REIT is Weingarten Realty Investors (WRI). In terms of utility companies, I like DPL, Inc (DPL) and Equitable Resources Inc. (EQT).

There is a lot of discussion regarding the Technology sector and whether or not value investors should begin buying. We still view technology as an “AAS Recommended Sell” sector. However, it should be noted that Microsoft Corp. (MSFT) was upgraded to an “AAS Recommended Buy” this morning along with Cerner Corp. (CERN).

Other notable upgrades include: Scholastic Corp. (SCHL); Amgen Inc. (AMGN); AmerisourceBergen Corp. (ABC); Stryker Corp. (SYK); Reynolds & Reynolds Co. (REY) and The Great Atlantic & Pacific Tea Company Inc. (GAP).

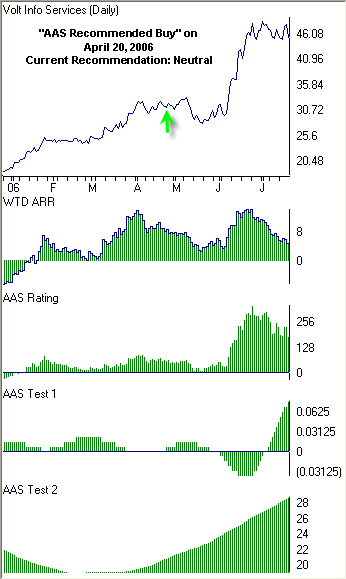

Seeing is believing. With that in mind, each week I’ll provide a graph of six holdings from the Alpha Advisor Service, LLC newsletter. Included in the newsletter, which is provided to our subscribers on Tuesday and Thursday mornings, is the Top Ten page. The Top Ten page is broken down into six groups of equities that include: Long Stocks, Short Stocks, Exchange Traded Funds, Fidelity Select Funds, ProFunds Funds and Rydex Funds. We include ten equities within each group, ranked first by the current AAS Recommendation, and then by the AAS Rating Score. Those that are “AAS Recommended Buys” and that have the highest AAS Rating Scores are at the top. The graphs below represent the top holdings within the six groups as of Friday, July 14, 2006. I’ve included the date that the equity was most recently labeled an “AAS Recommended Buy,” or in the case of the short-sell group, an “AAS Recommended Sell" as well as the current recommendation of each security. Volt Information Service (VOL) was the highest rated stock as of July 14th. This company shifted from a "Neutral" rating to an "AAS Recommended Buy" on April 20, 2006. Since VOL became an "AAS Recommended Buy," is has gone up nearly 40% as of the close on July 21st. Currently, VOL is an "AAS Recommended Neutral," which basically means "Hold." The technicals have weakened somewhat over the last few days, but they have not deteriorated to the point where a Sell recommendation is justified.

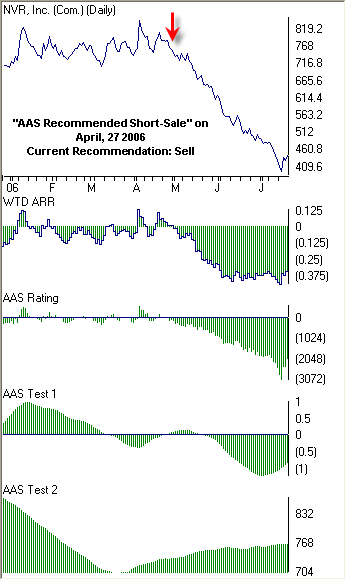

The lowest rated stock on July 14th was NVR, Inc. (NVR). The "Short Stock" group included in the AAS Top Ten page is comprised of those securities that are "AAS Recommended Sells" that have the lowest AAS Rating Scores. We published an "AAS Recommended Sell" of NVR on April 27, 2006. As of July 14th, the AAS Rating Score was -2599.62. From the initial "AAS Sell Recommendation" through the close on July 21st, NVR was down -44%. Currently, NVR is still an "AAS Recommended Sell." Shorting stocks, although profitable if done correctly, is risky business. There's no need to do it unless you have the experience, knowledge, and capital to cover your short if needed. QMA does not short stocks for its clients and AAS does not recommend the practice to its subscribers.

The iShares Cohen and Steers Realty Majors ETF (ICF) was the highest rated Exchange Traded Fund on July 14th with an AAS Rating Score of 24.37. ICF was up-graded to an "AAS Recommended Buy" on June 29, 2006. Since then, ICF has seen a modest 1.64% price increase. Currently, ICF remains an "AAS Recommended Buy."

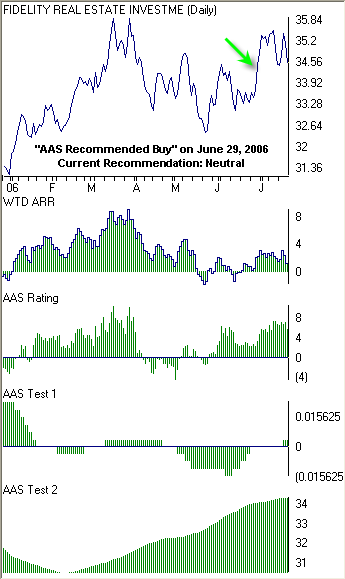

Real Estate, along with Utilities, and more recently Healthcare, have been the only sectors rated "AAS Recommended Buy." That's why it was no suprise that the Fidelity Real Estate Investment Fund (FRESX) was the highest rated Fidelity Select mutual fund as of July 14th. This ETF was also upgraded to an "AAS Recommended Buy" on June 29, 2006. Since then, FRESX has gone up by 0.23% and is an "AAS Recommended Neutral" equity.

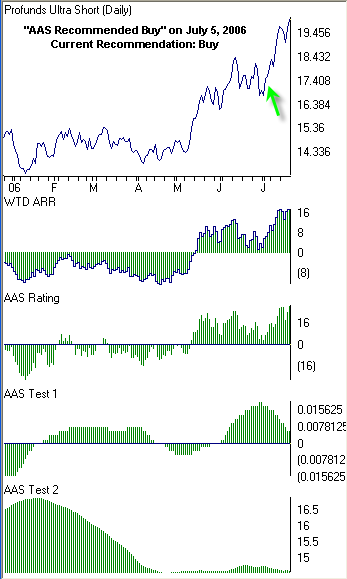

The ProFunds Ultra Short OTC Fund (USPIX) was the highest rated ProFund mutual fund on July 14th with an AAS Rating Score of 27.12. This fund is leveraged to correspond to twice the inverse of the NASDAQ 100 Index. In times of high volatility, tech stocks often under-perform, and this recent range-bound market is no exception. This fund was upgraded to an "AAS Recommended Buy" on July 5th when the price was 17.48. As of Friday, USPIX closed at 20.02 for a gain of 14.5% and currently remains an "AAS Recommended Buy."

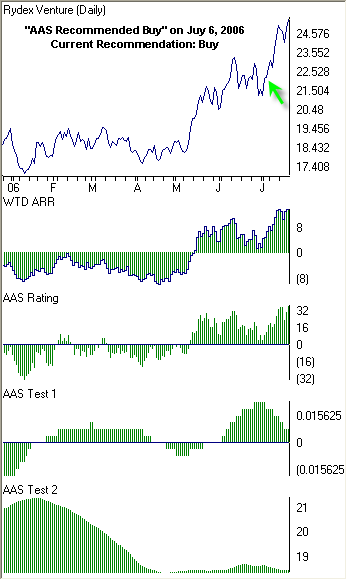

Similar to above, the Rydex Inverse Dynamic OTC Fund (RYVNX) was the highest rated Rydex mutual fund on July 14th with an AAS Rating Score of 33.83. This fund was upgraded to an "AAS Recommended Buy" one day later than its ProFund counterpart. On July 6th the closing price of RYVNX was 22.19 and as of Friday, the close was 25.35 for a gain of over 14%. RYVNX is still an "AAS Recommended Buy."

The 21-Day Breadth, 21-Day Volume, On-Balance Volume %, MACD and 15-Day Relative Strength indicators that I look at daily continue to illustrate the range bound market that we’re currently faced with. The only indicator that remained bullish was the 15-Day Stochastic. This indicator takes the close of the Dow Jones Industrial Average and subtracts from it the lowest DJIA close over the last fifteen days. That value is then divided by the highest DJIA close minus the lowest DJIA close over the same fifteen days. A three day moving average smoothes the value. Normally, when this value moves from below twenty to above twenty it is considered a buy signal. Conversely, when it moves from above eighty to below eighty that indicates a sell signal. Despite yesterdays broad-based reversal, the 15-Day Stochastic increased from 20.20 to 30.88 overnight. This indicator is only one of several I use daily and by no means dictates my overall market call. But I always pay attention to the black sheep, if for no other reason than to observe its movement.

These indicators, much like the market itself, fluctuate almost daily from slightly bearish to slightly bullish. This brings to focus a very obvious rule that trend followers observe, but one that many investors fail to accept. Market reversals or trends, much like Rome, are not built in a day. I’m not implying that comments from the Fed, or strong earnings reports, or war in the Middle East cannot impact the market. I’m simple saying that it takes more to resuscitate a range-bound market than some investors realize.

So, where does that leave us now? Long or short? Tech or Energy? Foreign or Government Bond? I think the best course of action is first to relax, and second not to over react. Don’t swing at every curve ball the market throws your way. At this point, a lot more money can be lost than can be made. We’re still advising extreme caution and an asset allocation of between 0% and 25% equities. The total universe of stocks, ETF and funds which Alpha Advisor Service, LLC reviews on a daily basis is 1,745. Of those reviewed, 216 are rated "Buy," 972 are rated "Sell" and 557 "Neutral." With over four times as many “Sells” as “Buys,” we’re not overly excited about the odds facing us at the moment.

Real Estate, Utilities and Healthcare are still “AAS Recommended Buys.” Financials and Financial Services are doing well this week. I’d like to see financials take the lead and help guide the market, but that has yet to happen, although this week might have been the beginning. Which sectors are worth avoiding currently? Semiconductors and Networking are the lowest rated, but Biotechnology and Transports are not far behind. Despite the reversal, there are some equities that managed to be up-graded to “AAS Recommended Buys” this morning. There are forty-seven utility stocks currently rated as “AAS Recommended Buys,” by far more than any other sector. The five new ones are: Duquesne Light Holdings Inc. (DQE), Edison International (EIX), Pinnacle West Capital Corp. (PNW), Laclede Group Inc. (LG) and Vectren Corp. (VCE).

Telecommunication is a sector I briefly discussed yesterday as one that tech-craving investors might look at. Interestingly enough, Qwest Communications International Inc. (Q) was also upgraded to an “AAS Recommended Buy” this morning.

Healthcare, a relatively newly upgraded sector, presents almost as many worthy equities as the Utilities sector. Two stocks that I noticed are Community Health Systems Inc. (CYH) and HCA Inc. (HCA). These are hospital related healthcare stocks, which is a conservative play in a time of uncertainty and volatility.

Fed Chairman Bernanke sparked a huge rally across the boards yesterday by testifying to Congress that inflation is now under control and that a recession was unlikely. Wall Street scaled-back the probability of another quarter point rate hike in August from 90% to 68%, as indicated by Fed Fund futures contracts. A strong earnings report by JP Morgan (JPM) further motivated the Dow Jones Industrials index to the largest percentage gain since April 2002. Solid after-the-close reports by Apple Computer (AAPL), Motorola (MOT) and eBay (EBAY) should balance with the not-so-good quarterly results of Intel (INTC), Qualcomm (QCOM) and especially Yahoo! (YHOO) which is down nearly 22%. The S&P 500 Index jumped 1.9% on the day, with Southwest Airlines (LUV) the biggest gainer at 9.3%. Before the bell futures traded near fair value indicating a relatively flat open.

Despite the broad-based rebound yesterday, not all news was good news. The core Consumer Price Index (CPI) rose 0.3% in June, steeper than the 0.2% consensus estimates. Additionally, the year-over-year core CPI was up 2.6%, the first time that rate has been above 2.4% since the spring of 2002. Finally, groundbreaking on new homes in June fell 5.3% from the month before to an annual rate of 1.85 million units, lower than the expected rate of 1.9 million.

The biggest question for investors alike is what does yesterday mean? Should this be interpreted as the beginning of a rally, or was yesterday the result of short-covering by investors expecting a downturn? The big board only saw volume at 1.8 billion shares, hardly enough to indicate a trend reversal. Yet several of the technical indicators we follow made huge reversals including the 21-Day Breadth, 21-Day Volume, On-Balance Volume %, MACD, 15-Day Stochastic and 15-Day Relative Strength indicators. Additionally, all three Put / Call Ratios retreated.

I think ordinarily in a down-trending market, a day like yesterday might be enough to spark a reversal. But unfortunately we’re not in a trending market, we’re range bound, a condition dictated by traders and much too volatile for us. In fact, yesterday’s activity does little to change our opinion of the markets. We’re still advising extreme caution and an asset allocation of between 0% and 25% equities. The total universe of stocks, ETF and funds which Alpha Advisor Service, LLC reviews on a daily basis is 1,745. Of those reviewed, 234 are rated "Buy," 765 are rated "Sell" and 746 "Neutral."

Despite yesterday, Real Estate, Utilities and now Healthcare are the only sectors rated as “AAS Recommended Buys.” Financials, Financial Services and yes, Telecommunication, are all having a good week, as evident by their increasing AAS Rating Scores, yet they are still unable to pass the indicators needed to be upgraded to “AAS Recommended Buys.” Equities within the technology sectors are always volatile, but with the strong earnings statements yesterday coupled with those of Google (GOOG), Microsoft (MSFT) and Advanced Micro Devices (AMD) on the docket, value investors want to watch the Telecomm and even Software sectors closely. It might not be a bad idea to invest in one or two newly upgraded tech stocks, at least for the short term. Possible candidates include Cincinnati Bell Inc. (CBB) and Komag Inc. (KOMG).

Finding and applying alpha to a portfolio is no longer limited to wealthy hedge fund investors and institutions. In fact, any private or professional investor can develop, manage, and benefit from an investment portfolio based on our approach to alpha. And more importantly, investors can do so without losing value to high management fees. This blog will include selected data from the Alpha Advisor Service, LLC newsletter, a tool designed especially for those investors looking to find alpha.

Location: Charlotte, North Carolina, United States

I'm a quantitatively-focused professional with a passion for all financial markets and instruments. I incorporate technical analysis and trend following with top-down "black-box" security selection to generate alpha.

The material provided by Portable Alpha Daily is for general informational purposes only. This information is not intended as investment advice, as an offer or solicitation of an offer to sell or buy, or as an endorsement, recommendation or sponsorship of any company, security or fund. The contents of this website have been compiled from original and published sources believed to be reliable, but are not guaranteed as to accuracy or completeness. Pursuant to the provisions of Rule 206(4)-1 of the Investment Advisors Act of 1940, Portable Alpha Daily advises all visitors to recognize that they should not assume that recommendations made in the future will be profitable or will equal the performance of past recommendations. The visitor accepts the responsibility of his or her own investment research and decisions, and should seek the advice of a qualified securities professional before making any investment.